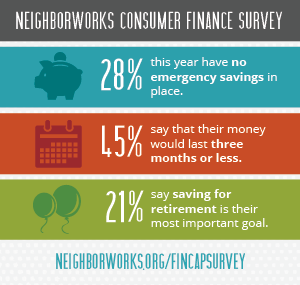

America is in the midst of a savings crisis. Approximately one of every two American households are considered “financially fragile,” according to the Federal Reserve Bank, whose 2016 study found that 47 percent of respondents to a national survey could not cover an unexpected $400 expense without going into debt.

The outlook is particularly dire for those with low incomes and communities of color. Forty-two percent of households of color live in asset poverty (with savings and assets insufficient to carry them over during a financial emergency) compared to 20 percent of whites. Alarmingly, 25 percent of black households would have less than $5 if they liquidated all of their assets. Likewise, a NeighborWorks America study found that only 30 percent of families with annual incomes less than $20,000 had emergency savings.

Statistics on the depth and breadth of the savings crisis may vary, but one fact is crystal clear: For many Americans, unexpected expenses cause immediate hardship, often triggering a downward spiral from which it is hard to recover. For millions in this country, an unexpected event—like missing work for an extended period due to illness or car troubles—can lead to financial ruin when combined with the absence of a financial safety net.

Statistics on the depth and breadth of the savings crisis may vary, but one fact is crystal clear: For many Americans, unexpected expenses cause immediate hardship, often triggering a downward spiral from which it is hard to recover. For millions in this country, an unexpected event—like missing work for an extended period due to illness or car troubles—can lead to financial ruin when combined with the absence of a financial safety net.

NeighborWorks America has identified access to emergency savings as a critical need of clients participating in its financial-coaching program. Thus, it contacted EARN to see if we could work together to design a program that would help its network members’ clients establish a habit of savings and build a $500 emergency fund.

Together, we designed a 2:1 matched-savings program that leverages EARN’s technology platform to integrate flexible emergency savings into NeighborWorks’ financial coaching program. NeighborWorks selected 17 sites to participate in the pilot, with the goal of helping 350 families save their first $500. Over the course of the year, we will measure the results of the pilot to determine the impact of matched savings on household finances, coaching retention and housing stability.

A recent report from the Urban Institute concludes that families with a savings cushion as little as $250 to $749 are less likely to be evicted, miss a housing or utility payment, or forced to rely on public benefits after a job loss, health issue or large income drop.

EARN currently has more than 50 nonprofit partners that are integrating savings solutions into a broad range of services, including affordable housing, financial coaching and counseling, and workforce development. Among the benefits: Our savings program is simple and easy for savers to use, empowers them to save anytime anywhere, and allows partner agencies to integrate savings into their work with low administrative costs. Partners also gain access to valuable data on clients’ savings behavior, allowing them to make informed programmatic decisions.

Income alone will not solve the challenges facing low-income families working to escape poverty and attain lasting financial security. A savings habit, and the stability it brings, is equally important: Regular savings is one of the three predictors of whether low-income people will be able to rise above the bottom 20 percent of the economy.

03/21/2017